Initiating Coverage | Footwear

September 1, 2016

Mirza International

BUY

CMP

`84

Red Tape to escalate the green print

Target Price

`113

Mirza International Ltd (MIL) is engaged in manufacturing and marketing leather and

Investment Period

12 Months

leather footwear. It exports its products to the European Union, Germany, the United

Kingdom, the United States, Italy, and France among other geographies. Its brands

Stock Info

include Red Tape and Oaktrak.

Sector

Footwear

Strong growth in domestic branded segment to drive overall growth: In the branded

Market Cap (` cr)

1,011

domestic segment, we expect the company to report a ~24% CAGR over FY2016-18E

to `346cr. We anticipate strong growth for the company on the back of (a) the

Net Debt (` cr)

213

company’s wide distribution reach through its 1,000+ outlets including 120 exclusive

Beta

1.6

brand outlets (EBOs) in 35+ cities and the same are expected to reach 200 over the

52 Week High / Low

145/83

next 2-3 years and (b) strong branding (Red Tape) in the shoes segment. Further, MIL

Avg. Daily Volume

100,469

is enhancing its brand visibility owing to higher ad spend in FY2017. MIL has doubled

Face Value (`)

2

its ad spend over the last five years; ad spends as a proportion of branded product

sales now stand at 9-10%.

BSE Sensex

28,452

Strong global footprint: MIL’s major export revenue comes from the UK

(73%),

Nifty

8,786

followed by the US (14%) and the balance from ROW. Export constitutes ~75% of the

Reuters Code

MIRZ.BO

company’s total revenue. The company is reasonably insulated in terms of client

Bloomberg Code

MRZI.IN

concentration. Its clients include ASDA, River Island, Matalan, ASOS, Elan Polo, and

Steve Madden among others. In the UK, the company has a market share of ~25% in

the men’s leather footwear mid-segment category. We expect the company to report

Shareholding Pattern (%)

healthy growth over the next 2-3 years on back of recovery in the UK market, strong

Promoters

73.8

growth in the US market and with it tapping newer international geographies like the

MF / Banks / Indian Fls

0.3

Middle East countries.

FII / NRIs / OCBs

0.5

Genesis Footwear merger to boost margins: In FY2016, the company acquired

Genesis Footwear which has a better margin profile than it. The deal resulted in MIL’s

Indian Public / Others

25.4

EPS increasing by ~4% and ROE improving from 15.9% to 17.5%. Further, due to this

merger, the company’s capacity has increased from 5.4mn to 6.4mn units. During FY2016,

the company reported net sales of `90cr, EBITDA margin of ~29%, and PAT of `20cr.

Abs.(%)

3m

1yr

3yr

Outlook and Valuation: We expect MIL to report a net revenue CAGR of ~11% to

Sensex

6.7

8.3

50.7

~`1,148cr over FY2016-18E on back of strong growth in domestic branded sales

MIL

(13.4)

(24.4)

318.2

(owing to aggressive ad spend and addition in the number of EBOs & multi-brand

outlets [MBOs]) and healthy export revenues. On the bottom-line front, we expect a

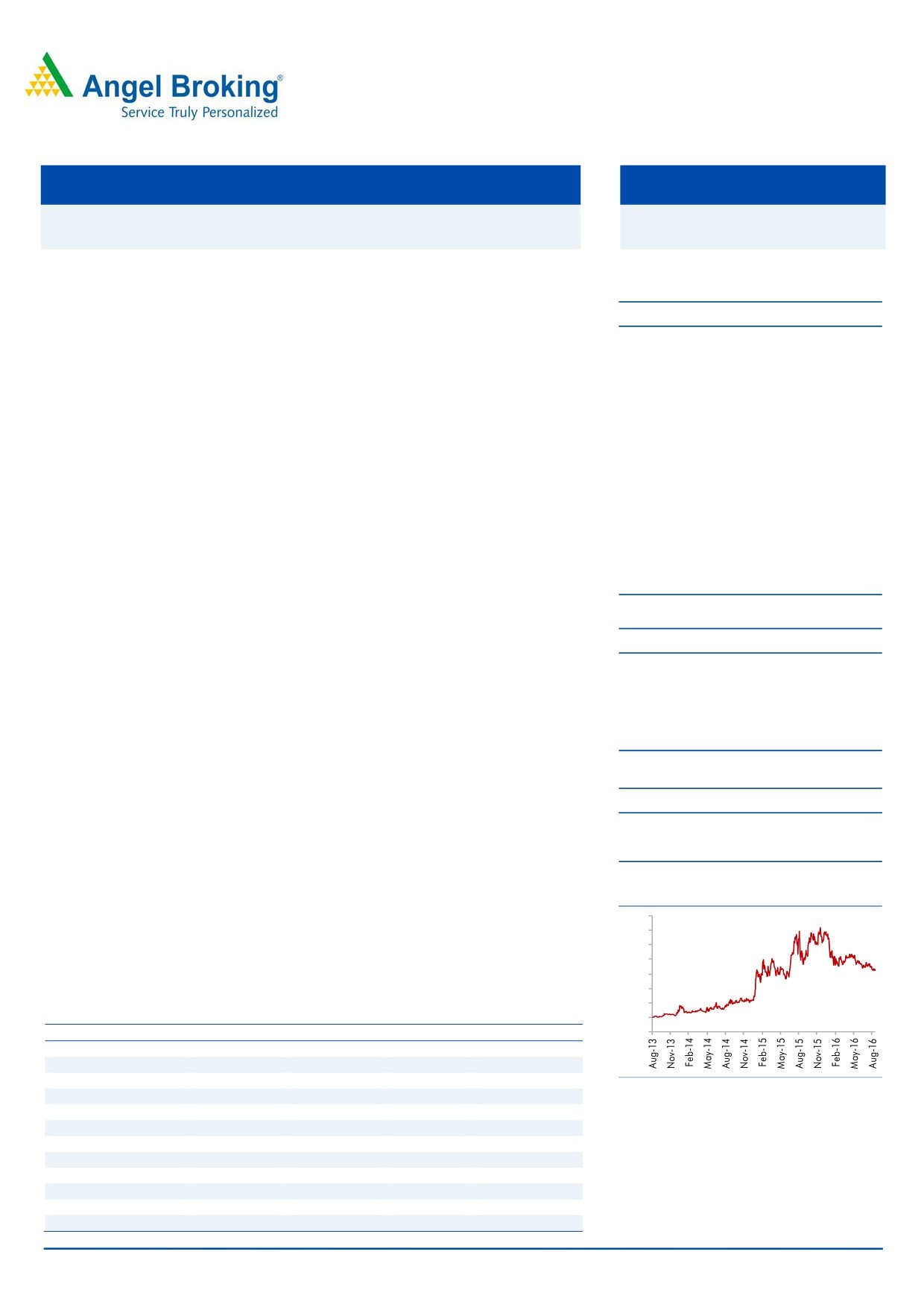

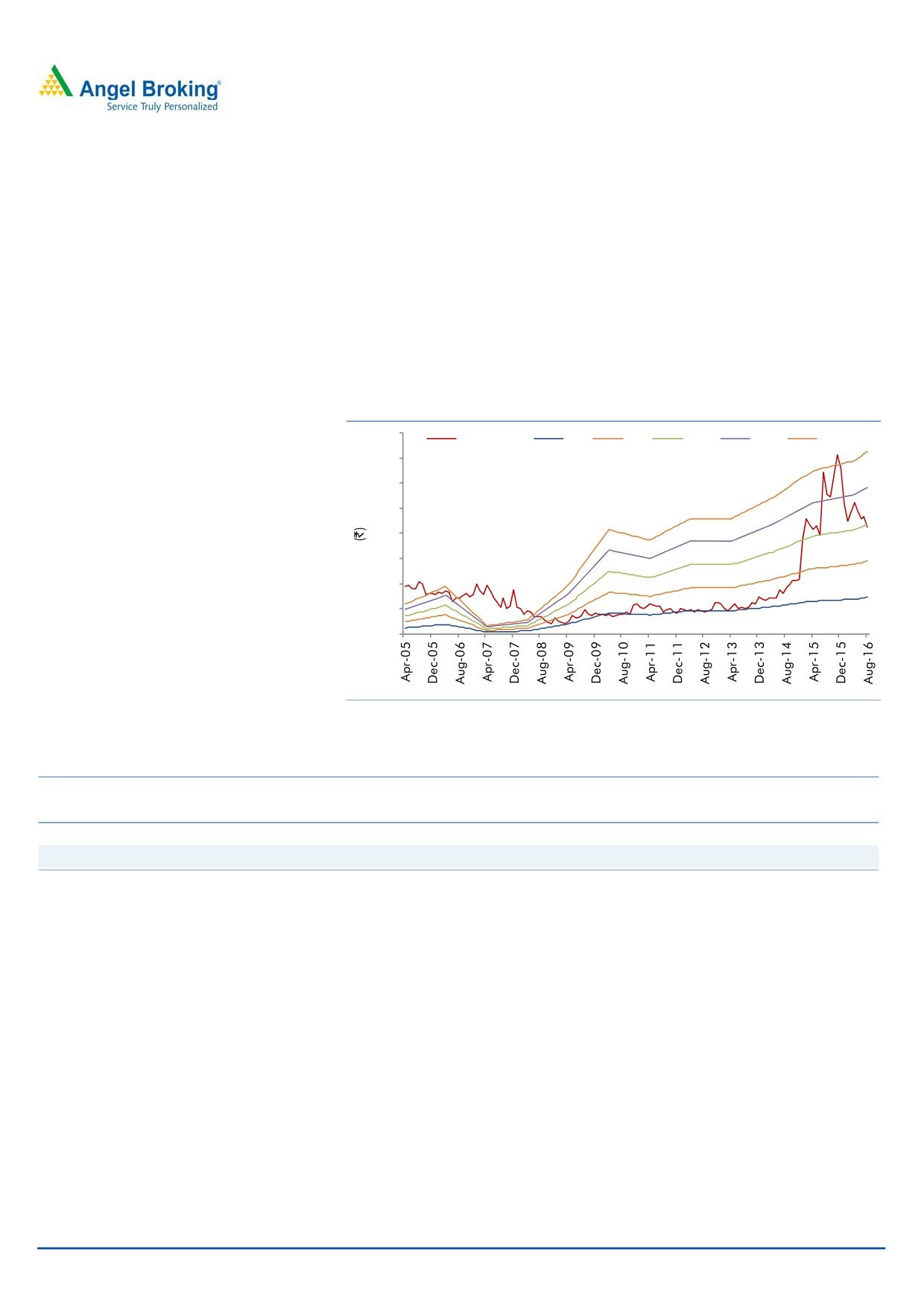

3-year price chart

CAGR of ~11% to `97cr over the same period on the back of margin improvement.

160

At the current market price of `84, the stock trades at a PE of 12.2x and 10.5x its

140

120

FY2017E and FY2018E EPS of `6.9 and `8.0, respectively. We initiate coverage on the

100

stock with a Buy recommendation and target price of `113 based on 14x FY2018E EPS,

80

indicating an upside of ~34% from the current levels.

60

40

Key financials

20

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

0

Net sales

919

927

1,024

1,148

% chg

29.9

0.9

10.4

12.2

Net profit

51

78

83

97

Source: Company, Angel Research

% chg

51.2

78.1

83.0

96.7

EBITDA margin (%)

15.5

18.5

18.0

18.0

EPS (`)

4.3

6.5

6.9

8.0

P/E (x)

19.8

12.9

12.2

10.5

P/BV (x)

3.3

2.4

2.1

1.7

RoE (%)

16.4

18.5

16.6

16.3

RoCE (%)

22.3

22.6

21.5

21.5

Amarjeet S Maurya

EV/Sales (x)

1.3

1.3

1.2

1.0

022-39357800 Ext: 6831

EV/EBITDA (x)

8.6

7.1

6.5

5.8

Source: Company, Angel Research, Note: CMP as of September 1, 2016

Please refer to important disclosures at the end of this report

1

Mirza International | Initiating Coverage

Key investment arguments

Strong growth in domestic branded segment to drive overall growth

In the branded domestic segment, we expect the company to report a ~24%

CAGR over FY2016-18E to `346cr. We anticipate strong growth for the company

on the back of (a) the company’s wide distribution reach through its 1,000+

outlets including 120 exclusive brand outlets (EBOs) in 35+ cities and the same

are expected to reach 200 over the next 2-3 years and (b) strong branding (Red

Tape) in the shoes segment. Further, MIL is enhancing its brand visibility owing to

higher ad spend in FY2017. MIL has doubled its ad spend over the last five years;

ad spends as a proportion of branded product sales now stand at 9-10%.

Exhibit 1: Healthy domestic growth expected

400

90

79.4

77.4

74.4

350

80

69.1

69.4

69.4

66.0

70

300

60

250

50

200

40

150

30

100

20

50

10

143

160

201

210

235

292

357

0

0

FY2012

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Net domestic sales

Brand sales as % of Domestic sales

Source: Company, Angel Research

Exhibit 2: Company’s historical ad spend trend

Exhibit 3: Distribution channel profile

13.3

200

14.0

12

12.4

175

180

12.0

11.2

10.7

10

160

10.0

140

8

8.0

120

6

5.6

100

6.0

80

4

60

60

4.0

60

2

2.0

40

20

0.0

0

FY2011

FY2012

FY2013

FY2014

FY2015

0

Ad spend

% of domestic branded sales

Shop in Shop

EBO (owned)

EBO (Franchise)

Source: Company, Angel Research

Source: Company, Angel Research

September 1, 2016

2

Mirza International | Initiating Coverage

Exhibit 4: REDTAPE brand profile - Footwear, Apparel, Accessories etc.

Source: Company, Angel Research

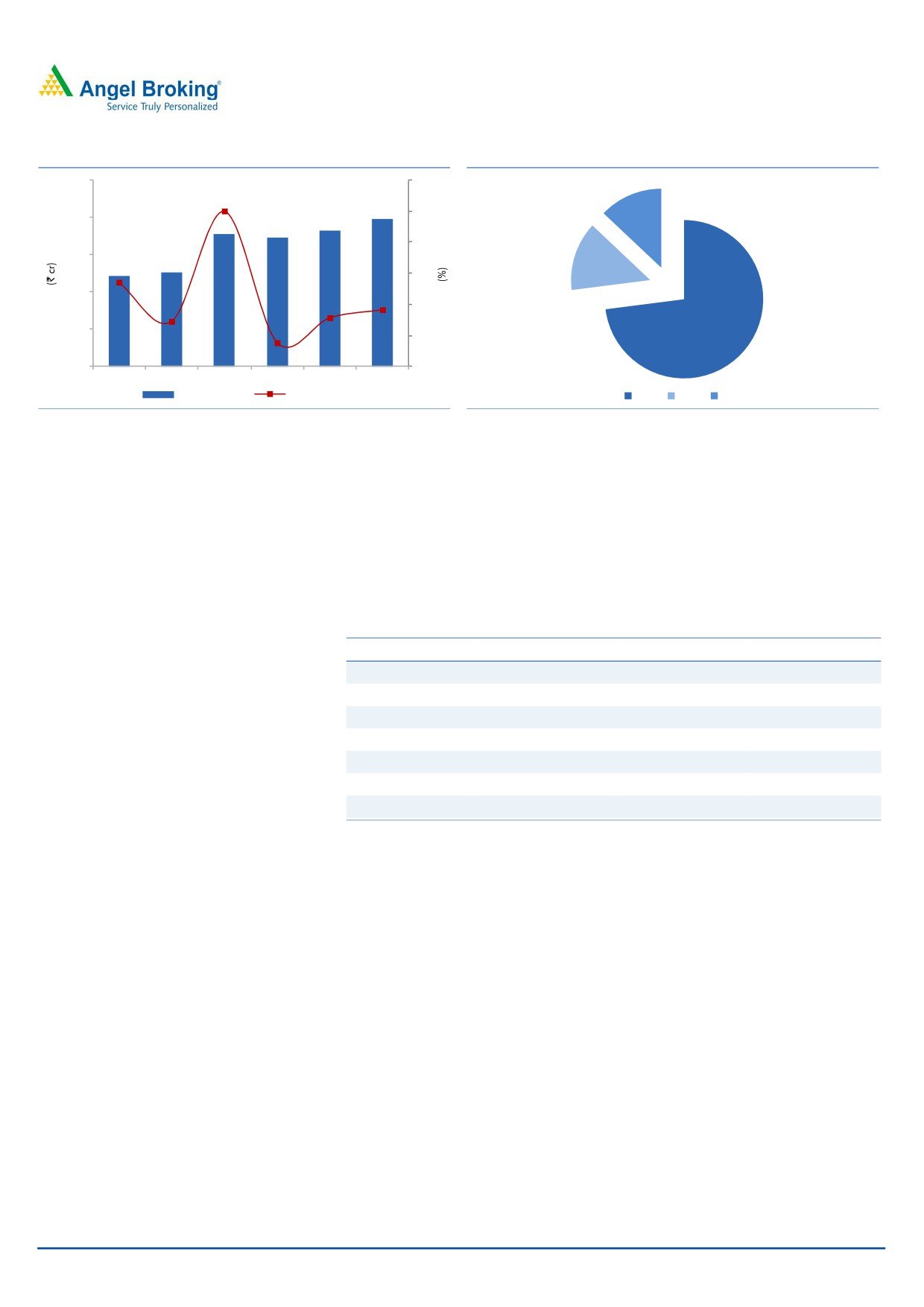

Strong global footprint to drive overall growth

MIL exports its products to the European Union, the United Kingdom, the United

States, Italy, and France, among other geograhies. The company’s major export

revenue comes from the UK (73%), followed by the US (14%) and the balance from

ROW. Exports constitute ~75% of the company’s total revenue. The company is

reasonably insulated in terms of client concentration. Among the company’s clients

are ASDA, River Island, Matalan, ASOS, Elan Polo, Steve Madden etc. In the UK,

the company has a market share of ~25% in the men’s leather footwear mid-

segment category. On the revenue front, the company reported a ~14% CAGR

over the past four years and is expected to generate healthy growth in the coming

few years as well on back of recovery in the UK market, strong growth in the US

market and with it looking to penetrate further across international geographies

like the Middle East countries.

Exhibit 5: Strong Distribution network in US & UK and also reach in 30

countries worldwide

MBO Stores in USA

MBO Stores in UK

500+

1200+

Source: Company, Angel Research

September 1, 2016

3

Mirza International | Initiating Coverage

Exhibit 6: Historical and Projected export trend

Exhibit 7: Export revenue break-up in FY2016

1000

50

13%

39.9

40

800

30

600

14%

20

17.1

400

8.2

10

5.6

4.5

200

0

(2.4)

73%

0

(10)

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Export Revenue

yoy growth (%)

UK

US

ROW

Source: Company, Angel Research

Source: Company, Angel Research

Genesis Footwear merger to boost margins

In FY2016, the company acquired Genesis Footwear which has a better margin

profile than it. The deal resulted in MIL’s EPS increasing by ~4% and ROE

improving from 15.9% to 17.5%. Further, due to this merger, the company’s

capacity has increased from 5.4mn to 6.4mn units. During FY2016, the company

reported net sales of `90cr, EBITDA margin of ~29%, and PAT of `20cr.

Exhibit 8: Financial data of MIL and Genesis Footwear

Mirza International

Genesis footwear

Merged company

Sales

927

90

927.17

Operating Profit

146

26

171.98

Margin (%)

15.7%

28.9%

18.5%

PAT

58

20

78.09

ROE

15.9%

23.8%

17.5%

No of share cr

9.27

3.0

12.03

EPS

6.3

6.7

6.5

Source: Company, Angel Research

About Genesis Footwear: Genesis Footwear is engaged in footwear manufacturing

and has an in-house design studio and R&D facility. Its manufacturing plant is fully

exempt from excise payment as it’s situated in the Kashipur, Uttrakhand, tax free

zone. Before the merger, the company used to buy raw materials from MIL and

also sell shoes to MIL.

September 1, 2016

4

Mirza International | Initiating Coverage

Outlook and Valuation

We expect MIL to report a net revenue CAGR of ~11% to ~`1,148cr over

FY2016-18E on back of strong growth in domestic branded sales (owing to

aggressive ad spend and addition in the number of EBOs & multi-brand outlets

[MBOs]) and healthy export revenues. On the bottom-line front, we expect a CAGR

of ~11% to `97cr over the same period on the back of margin improvement. At

the current market price of `84, the stock trades at a PE of 12.2x and 10.5x its

FY2017E and FY2018E EPS of `6.9 and `8.0, respectively. We initiate coverage on

the stock with a Buy recommendation and target price of `113 based on 14x

FY2018E EPS, indicating an upside of ~34% from the current levels.

Exhibit 9: One year forward PE Chart

160

Share Price

4x

8x

12x

16x

20x

140

120

100

80

60

40

20

0

Source: Company, Angel Research

Exhibit 10: Peer Comparison

Market Cap

EPS

PE (x)

EV/EBITDA (x)

ROE (%)

FY16

FY17

FY18

FY16

FY17

FY18

FY16

FY17

FY18

FY16

FY17

FY18

MIL

1,021

6.5

6.9

8.0

12.9

12.2

10.5

7.1

6.5

5.8

18.5

16.6

16.3

Bata

6,862

11.2

12.9

15.1

47.8

41.5

35.5

24.9

22.5

19.7

13.2

14.1

15.6

Source: Company, Angel Research

Downside risks to our estimates

Any slowdown in global economy could hurt the company’s revenue (75% of

revenue comes from exports).

Volatility in USD and Euro exchange rate against INR can have negative

impact on margins.

September 1, 2016

5

Mirza International | Initiating Coverage

Company Background

MIL is an India-based company engaged in manufacturing and marketing leather

and leather footwear. The company’s operations are segmented as the Footwear

division and the Tannery division. Its Tannery division manufactures finished

leather from raw hides, wet blue and crust and the Footwear division manufactures

finished leather shoes. The company exports its products to the European Union,

Germany, the United Kingdom, the United States, Italy, and France, among other

geographies. It operates an in-house shoe production facility and a design studio

in London. Its brands include Red Tape and Oaktrak. The Red Tape brand’s

product portfolio includes men's footwear, women's footwear, shirts, jackets,

denims, tees, pants/shorts and accessories. Oaktrak is a brand of formal footwear

including casual and urban styles. Oaktrak is sold through independents, small

retailers and multiples.

Exhibit 11: Historical revenue mix

100

80

72

71

69

74

75

77

75

60

40

20

28

29

31

26

25

23

25

0

FY2012

FY2013

FY2014

FY2015

FY2016

FY2017E FY2018E

Domestic

Exports

Source: Company, Angel Research

September 1, 2016

6

Mirza International | Initiating Coverage

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Total operating income

644

707

919

927

1,024

1,141

% chg

16.3

9.9

29.9

0.9

10.4

11.4

Total Expenditure

528

586

776

755

839

935

Cost of Materials

370

404

548

504

570

636

Personnel

33

37

46

59

70

82

Others Expenses

125

145

182

192

200

217

EBITDA

116

122

143

172

184

205

% chg

37.2

5.1

17.1

20.6

7.1

11.4

(% of Net Sales)

18.0

17.2

15.5

18.5

18.0

18.0

Depreciation& Amortisation

20

22

25

26

29

31

EBIT

96

100

118

146

156

175

% chg

38.7

4.0

18.3

23.9

6.5

12.3

(% of Net Sales)

14.9

14.1

12.8

15.8

15.2

15.3

Interest & other Charges

32

32

39

32

34

34

Other Income

0

0

0

2

2

2

Recurring PBT

64

68

79

116

124

143

% chg

27.6

5.3

16.1

47.2

6.9

15.4

Prior Period & Extraord. Exp./(Inc.)

-

-

-

-

-

-

PBT (reported)

64

68

79

116

124

143

Tax

21

24

28

38

41

47

(% of PBT)

32.5

36.0

35.0

32.6

33.0

33.0

PAT (reported)

43

43

51

78

83

96

Add: Share of earnings of asso.

-

-

-

-

-

-

ADJ. PAT

43

43

51

78

83

96

% chg

43.4

43.4

51.2

78.1

83.0

95.8

(% of Net Sales)

6.7

6.1

5.6

8.4

8.1

8.4

Basic EPS (`

3.6

3.6

4.3

6.5

6.9

8.0

Fully Diluted EPS (`)

3.6

3.6

4.3

6.5

6.9

8.0

% chg

43.8

(0.1)

17.9

52.7

6.2

15.4

September 1, 2016

7

Mirza International | Initiating Coverage

Consolidated Balance Sheet

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

SOURCES OF FUNDS

Equity Share Capital

19

19

19

24

24

24

Reserves& Surplus

233

268

294

398

476

567

Shareholders Funds

251

287

313

422

500

591

Minority Interest

-

-

-

-

-

-

Total Loans

167

212

218

225

225

225

Deferred Tax Liability

21

23

15

15

15

15

Total Liabilities

440

521

545

662

740

831

APPLICATION OF FUNDS

Gross Block

371

441

489

551

591

631

Less: Acc. Depreciation

119

133

181

207

236

266

Net Block

252

308

308

344

356

365

Capital Work-in-Progress

30

7

3

3

3

3

Investments

1

1

1

1

1

1

Current Assets

224

300

346

421

499

588

Inventories

138

192

225

262

294

334

Sundry Debtors

33

42

43

63

76

91

Cash

4

6

6

11

30

48

Loans & Advances

44

56

67

74

87

103

Other Assets

5

3

5

10

11

13

Current liabilities

68

97

115

110

121

129

Net Current Assets

156

203

231

311

378

460

Deferred Tax Asset

2

2

3

3

3

3

Mis. Exp. not written off

-

-

-

-

-

-

Total Assets

440

521

545

662

740

831

September 1, 2016

8

Mirza International | Initiating Coverage

Consolidated Cashflow Statement

Y/E March (` cr)

FY13

FY14

FY15

FY16

FY17E

FY18E

Profit before tax

64

68

79

116

124

143

Depreciation

20

22

25

26

29

31

Change in Working Capital

(8)

(48)

(19)

(74)

(48)

(64)

Interest / Dividend (Net)

31

32

39

32

34

34

Direct taxes paid

(19)

(24)

(28)

(38)

(41)

(47)

Others

0

(0)

1

-

-

-

Cash Flow from Operations

89

48

97

61

97

96

(Inc.)/ Dec. in Fixed Assets

(58)

(54)

(59)

(63)

(40)

(40)

(Inc.)/ Dec. in Investments

-

-

-

-

-

-

Cash Flow from Investing

(58)

(54)

(59)

(63)

(40)

(40)

Issue of Equity

-

-

-

36

-

-

Inc./(Dec.) in loans

1

45

6

8

-

-

Dividend Paid (Incl. Tax)

(5)

(5)

(5)

(5)

(5)

(5)

Interest / Dividend (Net)

(36)

(33)

(40)

(32)

(34)

(34)

Cash Flow from Financing

(39)

8

(39)

7

(38)

(38)

Inc./(Dec.) in Cash

(8)

2

(1)

6

19

18

Opening Cash balances

12

4

6

6

11

30

Closing Cash balances

4

6

6

11

30

48

September 1, 2016

9

Mirza International | Initiating Coverage

Key ratios

Y/E March

FY13

FY14

FY15

FY16

FY17E

FY18E

Valuation Ratio (x)

P/E (on FDEPS)

23.3

23.3

19.8

12.9

12.2

10.5

P/CEPS

16.0

15.4

13.3

9.7

9.1

7.9

P/BV

4.1

3.6

3.3

2.4

2.1

1.7

Dividend yield (%)

0.5

0.5

0.5

0.5

0.5

0.5

EV/Sales

1.8

1.7

1.3

1.3

1.2

1.0

EV/EBITDA

10.1

10.0

8.6

7.1

6.5

5.8

EV / Total Assets

2.3

2.0

1.9

1.6

1.4

1.2

Per Share Data (`)

EPS (Basic)

3.6

3.6

4.3

6.5

6.9

8.0

EPS (fully diluted)

3.6

3.6

4.3

6.5

6.9

8.0

Cash EPS

5.3

5.4

6.3

8.6

9.3

10.5

DPS

0.4

0.4

0.4

0.4

0.4

0.4

Book Value

20.4

23.4

25.3

34.4

40.9

48.4

Returns (%)

ROCE

22.9

20.0

22.3

22.6

21.5

21.4

Angel ROIC (Pre-tax)

23.2

20.3

22.5

23.0

22.4

22.8

ROE

17.3

15.1

16.4

18.5

16.6

16.2

Turnover ratios (x)

Asset Turnover (Gross Block)

1.7

1.6

1.9

1.7

1.7

1.8

Inventory / Sales (days)

78

99

89

103

105

107

Receivables (days)

18

22

17

25

27

29

Payables (days)

27

35

33

30

30

28

WC cycle (ex-cash) (days)

69

86

74

98

102

108

September 1, 2016

10

Mirza International | Initiating Coverage

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Mirza International

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

September 1, 2016

11